Used by:

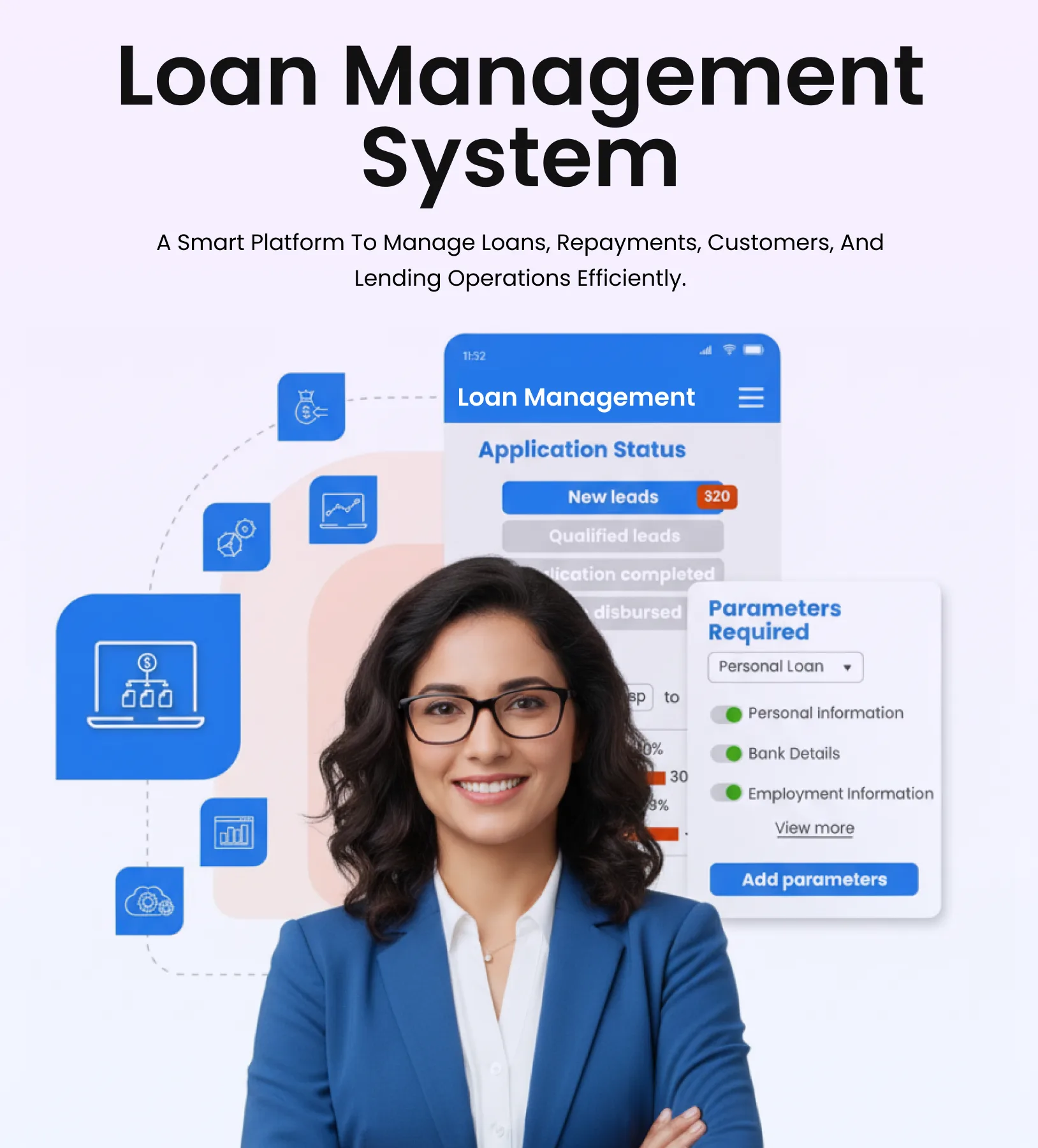

What is a Loan Management System?

Think of a loan management system like the control room for your entire lending business — after a loan is approved, everything that happens next lives here.

Here is a simple way to understand it

Imagine you lent ₹5 lakh to 500 different borrowers. Each borrower has a different loan amount, different EMI date, different interest rate, and different repayment history. Tracking all of that manually — in notebooks or Excel — is not just hard, it is dangerous. You will miss payments. You will miscalculate interest. You will fail audits.

A loan management system (LMS) is software that does all of that automatically. It knows who owes you how much, when they should pay, whether they paid on time, how much interest has accrued, and when a loan is getting risky — all in real time, for all 500 borrowers at once.

That is the core of what lending management software does. Everything else — compliance, reports, integrations — is built on top of that foundation.

The loan lifecycle — what your LMS handles

Every step from disbursement to closure, managed in one place.

Disbursement

Loan amount released to borrower. LMS records it instantly.

EMI Schedule

Auto-generates repayment calendar with correct interest split.

Collections

Tracks payments, sends reminders, flags late payers.

NPA Watch

DPD tracking, SMA classification, NPA alerts.

Closure

Foreclosure, NOC generation, bureau update.

Why Manual Loan Tracking is Slowly Hurting Your Business

Most lenders do not realize how much they are losing to bad processes — until an RBI audit happens or a large borrower defaults without warning.

You are calculating EMIs manually

Even one wrong formula in your Excel sheet can lead to wrong interest charges, borrower disputes, and potential legal trouble. A single error affects every row below it.

Your team is drowning in follow-ups

Calling borrowers for every overdue EMI takes hours every day. Meanwhile, accounts that need real attention are getting missed.

You find out about bad loans too late

NPA accounts do not appear overnight. The warning signs — delayed EMIs, partial payments, erratic behaviour — are there weeks before. Without software tracking them, you miss the window to act.

Compliance is always a scramble

Preparing MIS reports, bureau submissions, provisioning data — these take days when done manually. And one wrong filing can trigger regulatory action.

Loan restructuring is a nightmare

When a borrower needs a moratorium or rescheduling, recalculating the entire repayment schedule manually is both slow and error-prone.

You cannot see your full portfolio clearly

Which product is performing? Which geography is showing stress? Without a lending management software, these insights take days to compile — if they get compiled at all.

Core Features of a Modern Loan Management System

Here is what you should expect from any good loan management software — and what sets the best ones apart from the rest.

Automated EMI Calculation and Scheduling

The system auto-generates the full repayment schedule at disbursement — with accurate interest split, principal reduction, and due dates — for every loan product and every borrower. No manual math, no mistakes.

Real-Time Payment Reconciliation

Every payment received is matched to the correct loan account instantly. Whether it comes through UPI, NACH, cheque, or NEFT — the system records it, updates the ledger, and adjusts the outstanding balance in real time.

DPD Tracking and NPA Management

Days Past Due (DPD) is tracked automatically for every loan. The system flags accounts approaching SMA-0, SMA-1, SMA-2, and NPA status — giving your collections team time to act before accounts turn bad.

Loan Restructuring and Rescheduling

When a borrower needs relief — moratorium, EMI reduction, tenure extension — the software recalculates the entire schedule automatically. No manual rework. The system handles even complex multi-product restructuring.

Portfolio Reports and MIS Dashboards

Get instant visibility into your entire loan book — by product, geography, aging bucket, or risk category. Custom reports for board packs, investor decks, or RBI submissions can be generated in minutes, not days.

Bureau Reporting and Credit Updates

The system automates credit bureau submissions (CIBIL, CRIF, Equifax, Experian) so borrower credit records are updated on time — protecting both your compliance standing and your borrowers' credit health.

Moratorium and Subvention Handling

Whether it is a COVID-like moratorium announced by RBI or a subvention scheme offered by a manufacturer, the system adjusts interest accrual and repayment schedules without manual intervention.

Accounting and ERP Integration

Connect your loan management software with your existing accounting tools — Tally, SAP, Oracle, or any custom general ledger. Every disbursement, interest accrual, and repayment flows through automatically, keeping books accurate.

Role-Based Access and Audit Trails

Set who can see what. Relationship managers see their borrower data. Branch managers see their branch. The audit trail captures every action, every change, every login — so you always know what happened and who did it.

One Loan Management System for All Your Loan Products

Whether you run a single loan product or fifteen, the best loan management software handles all of them from one place — with product-specific configurations and shared borrower data.

Each product can have its own interest rate logic, repayment structure, fee rules, and compliance workflow — all configured without writing code.

Built for Every Kind of Lender — Big or Small

Good loan management software should work just as well for a 5-person NBFC as it does for a large bank. Here is how different lenders use it.

Banks and Large NBFCs

Handle millions of loan accounts across branches and geographies. Need robust NPA management, multi-currency support, and real-time reconciliation at scale. The LMS manages peak volumes — some systems handle over 3,000 transactions per second.

Fintechs and Digital Lenders

Need API-first architecture to build custom borrower experiences. Loan management software connects with their apps via APIs, automating the entire post-disbursement journey without any manual intervention.

Microfinance Institutions

Manage JLG and SHG group loan structures, weekly EMI collections, field agent workflows, and rural borrower data — often in low-connectivity environments. The LMS must be flexible and mobile-friendly.

Loan Management Software for Small Business Lenders

SME lenders in India need software that handles GST-based underwriting, working capital loans, and trade finance — with quick configuration for new products. No large IT team needed.

Loan Software for Private Lenders

Individual lenders and small lending firms need simple, clean tracking — who owes what, when it is due, and how to document agreements properly. The right loan management application makes this effortless without a finance team.

Housing Finance Companies

Long-tenure home loans need accurate interest recalculation on floating rates, property collateral tracking, and detailed amortisation reporting for regulators like NHB.

Loan Origination System vs Loan Management System — What Is the Difference?

These two are often confused. They solve different problems. You usually need both — and they should talk to each other seamlessly.

| Feature / Function | Loan Origination System (LOS) | Loan Management System (LMS) |

|---|---|---|

| When it works | Before the loan is approved | After the loan is disbursed |

| Main job | KYC, credit scoring, underwriting, approval | EMI tracking, repayments, NPA management, closure |

| Who uses it | Sales, credit officers, underwriters | Collections, operations, compliance, finance |

| Key integrations | Bureau, KYC APIs, BRE, eSign | Core banking, accounting, payment gateways |

| Output | Loan sanction letter, disbursement instruction | Repayment history, NPA status, closure certificate |

| Can you run without the other? | Sort of — but your origination will be manual | Sort of — but your servicing will be manual |

| Best practice | Use both — tightly integrated — for a seamless end-to-end lending platform. | |

Why Loan Management Software in India Needs to be Different

Indian lending is not like lending anywhere else. The regulatory environment — RBI guidelines, NHB norms, SEBI rules, IRDAI requirements — changes frequently. Your loan management system needs to keep up automatically.

What Indian lenders need from their LMS

- SMA classification (SMA-0, SMA-1, SMA-2) as per RBI Master Circular

- NPA provisioning — standard, sub-standard, doubtful, loss category

- Automated bureau reporting to CIBIL, CRIF, Experian, Equifax

- Fair Practices Code compliance for collections and communication

- Interest calculation based on actual disbursement date (no pre-EMI shortcuts)

- GST on processing fees and penal interest handling

- KFS (Key Fact Statement) generation as per RBI mandate

- Reset of floating interest rates tied to EBLR or MCLR benchmarks

- Co-lending module for bank-NBFC partnerships per RBI framework

- Audit trails meeting IS Audit standards

What compliance automation saves you

- No more manual SMA reporting scrambles at quarter-end

- Bureau submissions on time — every month, automatically

- NPA provisioning calculated correctly for your P&L

- Interest rate reset applied to all eligible accounts in one click

- Moratorium or subvention changes reflect across all accounts instantly

- Borrower communication logs maintained for grievance redressal

- Regulatory reports (Form A, Form B, NHB returns) ready at button click

- No more last-minute firefighting before RBI inspections

How to Choose the Best Loan Management System for Your Business

Not every loan management software is the same. Here is a practical checklist — built from what real lenders care about — to help you evaluate options without getting lost in feature lists.

Configurability over customisation

You should be able to add a new loan product, change an interest rule, or modify a repayment

schedule yourself — through a UI, not by calling developers. The best loan management

systems give

this power to your operations team.

Ask the vendor: "Can our team configure a new product without IT help? How long does

it

take?"

API-first architecture

Your LMS does not live alone. It needs to talk to your core banking system, payment gateway,

accounting software, and bureaus. If the loan management software does not have a

documented,

well-maintained API layer, integrations will be painful and expensive.

Ask the vendor: "Do you have a public API documentation? How many live integrations

do you

have in India?"

Proven at your scale

A system that works for 5,000 loans may struggle at 500,000. Before you sign, ask for

references at

your expected loan volume — and find out what their peak TPS (transactions per second)

capacity is.

Ask the vendor: "Who is your largest customer in India? What volume do they run at?"

Compliance is built-in, not bolted-on

RBI guidelines change. A good loan management system in India should update its compliance

rules

with each regulatory circular — not require you to file a change request and wait 3 months

for the

next release.

Ask the vendor: "How quickly did you incorporate the last major RBI circular? How is

it

rolled out to customers?"

Cloud vs on-premise

Cloud-based loan management software is faster to deploy, cheaper to maintain, and updates

automatically. On-premise gives you full data control. For most lenders in India today —

especially

newer NBFCs and fintechs — cloud is the right call.

Ask the vendor: "Where is our data hosted? What is your SLA for uptime? Do you have a

data

centre in India?"

Real support, not just a ticketing system

When something goes wrong during collections on the 1st of the month, you need a real person

to

answer the phone — not an automated email saying your ticket has been logged.

Ask the vendor: "What is your average resolution time for P1 issues? Do we get a

dedicated

account manager?"

40%

Faster decision times with automated workflows

2×

Loan portfolio growth reported by users

~10%

Reduction in default accounts

3000 TPS

Peak transaction capacity

Loan Management Glossary — Terms Every Lender Should Know

If you are evaluating lending management software, these are the terms you will hear constantly. Here is what they actually mean — in plain English.

DPD — Days Past Due

The number of days a borrower has gone without making a scheduled payment. DPD-0 means paid on time. DPD-30 means 30 days overdue. Your LMS tracks this automatically for every account.

NPA — Non-Performing Asset

A loan where the borrower has not paid for 90+ days. Once classified as NPA, the lender must set aside provisions against it. Early DPD tracking helps you catch accounts before they reach NPA.

SMA — Special Mention Account

RBI's early warning system. SMA-0 = overdue 1–30 days. SMA-1 = 31–60 days. SMA-2 = 61–90 days. After SMA-2, the account becomes NPA. Your loan management software should flag SMA accounts automatically.

Moratorium

A temporary pause on loan repayments — either declared by RBI (like during COVID) or offered by the lender to distressed borrowers. Interest typically continues to accrue and is added back to the principal.

Subvention

An interest subsidy where a third party — usually a manufacturer or government scheme — pays part of the borrower's interest. Common in vehicle loans and affordable housing. Your LMS must track who pays what portion of interest.

Loan Restructuring

Changing the terms of a loan after disbursement — such as extending tenure, reducing EMI, or converting interest to principal. The loan management system recalculates the entire schedule when a restructuring is applied.

NACH — National Automated Clearing House

The RBI-mandated electronic system for recurring payments. Most lenders use NACH to auto-debit borrower accounts on EMI due dates. Your LMS should integrate with NACH for seamless collections.

Pre-closure / Foreclosure

When a borrower repays the full outstanding loan before the due date. The LMS must calculate the correct outstanding principal, waive/charge applicable fees, generate the closure statement, and update bureau records.

EBLR / MCLR

External Benchmark Lending Rate (EBLR) and Marginal Cost of Funds based Lending Rate (MCLR) are RBI-mandated benchmarks for floating rate loans. Your loan management software must reset interest rates automatically when these benchmarks change.

Everything You Want to Know About Loan Management Systems

These are the questions lenders ask us most often before choosing a loan management system. We have answered every one of them honestly.

A loan management system is software that automates everything that happens after a loan is disbursed — EMI scheduling, payment tracking, NPA classification, collections, compliance reporting, and loan closure. You need one because managing even a few hundred borrowers manually in spreadsheets leads to mistakes, missed payments, compliance failures, and a lot of wasted time. As your portfolio grows, the need only gets more urgent.

Any individual or organisation that lends money and wants to manage those loans properly. This includes banks, NBFCs, fintechs, microfinance institutions, housing finance companies, credit unions, cooperative societies, private lenders, and even small businesses that extend credit to their customers. There is no minimum size — if you have more than 50 active loans, a loan management application pays for itself quickly.

A Loan Origination System (LOS) manages the front-end of lending — collecting applications, running KYC, checking credit scores, underwriting, and approving loans. A Loan Management System (LMS) takes over after the loan is approved and disbursed — tracking repayments, managing EMIs, flagging delinquencies, and handling closures. Most serious lenders use both, connected together so data flows seamlessly from origination to servicing.

A good loan management system can handle personal loans, business and SME loans, gold loans, home loans, vehicle and EV loans, education loans, BNPL, microfinance, loan against property, loan against shares or mutual funds, agricultural loans, supply chain finance, and credit lines on UPI. Each product can have its own EMI logic, fee structure, and compliance workflow configured independently.

Yes. Loan management software for small businesses in India should be cloud-based (so no expensive servers are needed), easy to configure without a dedicated IT team, compliant with RBI and GST requirements, and capable of connecting with popular accounting tools like Tally. Many platforms now offer SME-specific modules with working capital loan templates, GST-linked underwriting, and simple dashboards that do not require finance expertise to operate.

Absolutely. Loan software for private lenders is increasingly available as cloud-based, subscription-based tools that are affordable even for individual lenders. Private lenders benefit from features like borrower records, repayment schedule tracking, automated reminders, and documentation — things that protect them legally and financially without needing a large team.

Implementation time depends on complexity. A simple cloud-based loan management application for a single loan product can go live in 2–4 weeks. A full-scale deployment for a large NBFC with multiple products, integrations, and data migration from a legacy system typically takes 2–4 months. The key is choosing a vendor with a proven implementation methodology and dedicated onboarding support in India.

Yes, most modern lending management software integrates with popular accounting tools — Tally, SAP, Oracle, QuickBooks, and custom general ledgers — through APIs or direct connectors. This means every disbursement, interest accrual, fee, and repayment flows into your accounting records automatically without manual journal entries.

A good loan management system in India automates several RBI compliance requirements: SMA classification (SMA-0, SMA-1, SMA-2), NPA identification and provisioning, bureau reporting to CIBIL and other credit information companies, Key Fact Statement (KFS) generation, interest rate benchmarking (EBLR/MCLR), and Fair Practices Code adherence for collections. This dramatically reduces the compliance burden on your operations team and the risk of regulatory penalties.

Yes — reputable cloud-based loan management software providers maintain ISO 27001 certification, SOC 2 compliance, and follow RBI's guidelines on data localisation (data must be stored in India). Data is encrypted in transit and at rest, access is role-based, and audit logs capture all activity. In many ways, a certified cloud platform is more secure than an on-premise setup maintained by an understaffed IT team.

Most loan management platforms support standard reports like portfolio aging reports, overdue and NPA reports, repayment history by borrower, DPD distribution, disbursement MIS, interest income accrual, branch-wise performance, and bureau submission files. The best systems also let you build custom reports using your own parameters — for investor packs, board presentations, or specific regulatory formats.

When a loan needs to be restructured — because of a borrower's financial difficulty, an RBI moratorium directive, or a subvention scheme change — the loan management software recalculates the entire repayment schedule based on the new terms. This includes adjusting EMI amounts, extending or shortening tenure, recapitalising accrued interest, and regenerating the amortisation schedule. It happens automatically, without manual recalculation.

Built by People Who Actually Understand Lending

We did not build a generic software platform and then add loan features. We built a loan management system from the ground up — with domain experts who have spent decades working inside banks and NBFCs in India and across the world.

"We were managing 40,000 accounts in Excel. Within 8 weeks of going live on the platform, we had real-time NPA visibility and our collections team stopped spending half their day on manual reconciliation. The system paid for itself in the first quarter."

Operations Head — Mid-size NBFC, Maharashtra

LET'S GET YOUR PROJECT STARTED!

Share your idea and we'll turn it into reality. Quick quotes and fast turnaround.